Another Leg in the Bitcoin & Reflation Trade?

An accommodative Fed and inflation still remaining high yet the market is in a deflationary risk-off environment

Over the past several weeks we have seen a lot in the market develop. We have seen the entire market sentiment shift from an inflation narrative to fears of growth slowdown and potential lockdowns from the Delta Variant. And extreme fears of Central Bank tightening have emerged.

For example, today (7/20/21) the 10 year yield crashed to below 1.15bps! This tweet sums it up well:

Updates from My Recent Article

In my recent article, “The DXY & An Incoming Federal Reserve Policy Error”, I outlined my current view and what to what watch out for. See below:

Market View (6/30/21)

What to Watch (6/30/21)

So somethings here I was wrong on which is the Fed has not shown hawkishness but rather a willingness to continue the current QE program. So interestingly, the market has front run the Fed. We have seen a flattening of the yield curve, a higher dollar (though not by much), and asset prices head downward (especially reflation stocks, XOP down 20% from June highs).

The market has shown the Fed how fearful it is of tapering and even the idea of tapering has caused a risk-off in markets. I tend to believe Powell is fearful of a December 2018 scenario and plans to stay the course.

So instead of the Fed being hawkish and that driving down markets, the market showed the Fed its hand. Tapering is not an option. And so we could be preparing for another leg of the reflation trade.

What to Watch Update

DXY

The DXY is at 93.1. And we are approaching the first target of 93.5. I begin doubt if we get target 2 at 94 but the market will show us when and if 93.5 is hit.

Yield Curve Flattening

Yield Curve - Current (Solid Green); 1 Month Ago (Yellow); 2 Months Ago (Dashed Green)

2-10s Spread

We have seen the yield curve continue to flatten. We have seen the 10 year yield fall 40 bps and the 30 year even more so.

Federal Reverses Hawkishness

We have seen the opposite of hawkishness. Last week, Jerome Powell said the following at a Congregational Meeting on July 14:

The U.S. job market "is still a ways off" from the progress the Federal Reserve wants to see before reducing its support for the economy, while current high inflation will ease "in coming months," Fed Chair Jerome Powell said in remarks prepared for delivery at a congressional hearing. Powell also once again stressed that the Fed will provide "advance notice" before announcing any changes to its asset purchase program.

- Reuters (here)

Job gains should be strong in coming months as public health conditions continue to improve and as some of the other pandemic-related factors currently weighing them down diminish.

- Jerome Powell

There was little in Fed Chair Jerome Powell's semi-annual monetary policy testimony to suggest that officials are changing their tune that the current surge in inflation will be largely transitory.

- Andrew Hunter, Senior U.S. Economist at Capital Economics

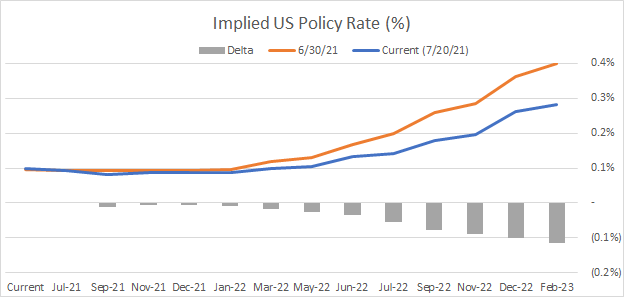

The Federal Reserve is strongly showing its willingness to be accommodative to financial assets and the economy.

And we can see the Fed reversing track from its hawkish stance in the implied policy rates from 6/30 to today.

One remaining question in my mind is what will come out of the Fed meeting at Jackson Hole in August. Most likely it’ll be what we have heard this month - continue to be accommodative to the economy.

Growth & Inflation & Fed Unwarranted QE

The most recent inflation print was 5.4%. And the below shows the ISM Manufacturing index implying CPI staying above 5% over the next 4 months. The below chart is ISM (4 month lead, Blue) vs CPI (Green).

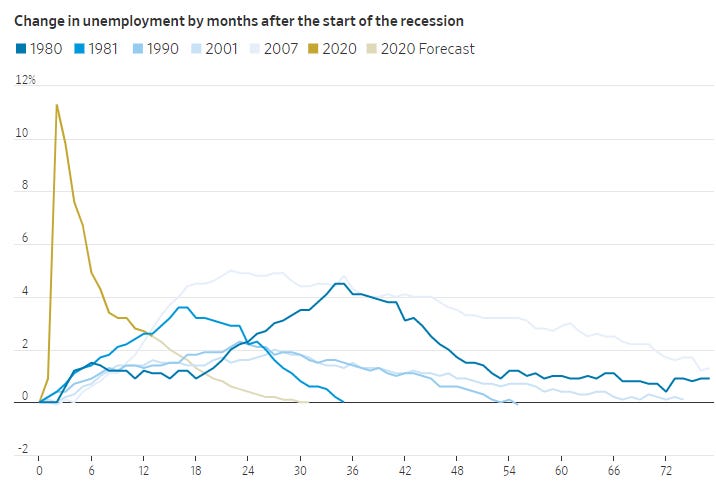

And unemployment is expected to drastically fall, faster than any other recession since 1980.

In summary, I am beginning to align with Stanley Druckenmiller’s view:

The American economy is back to prerecession levels of gross domestic product and the unemployment rate has recovered 70% of the initial pandemic hit in only six months, four times as fast as in a typical recession. Normally at this stage of a recovery, the Fed would be planning its first rate hike. This time the Fed is telling markets that the first hike will happen in 32 months, 2½ years later than normal. In addition, the Fed continues to buy $40 billion a month in mortgages even as housing is clearly running out of supply. And the central bank still isn’t even thinking about ending $120 billion a month of bond purchases.

- Druckenmiller (here)

I can’t find any period in history where monetary and fiscal policy were this out of step with the economic circumstances, not one.

- Druckenmiller

I am still a long term deflationist (outlined here) but over the next few months, there is strong reason to believe the reflation trade is back on.

Market View

I see market reaching the end of the yield curve flattening trade, higher dollar, and the deflationary trade in general. The trade setup from my recent article (here) accelerated faster than expected and it developed differently than I laid out. But the second piece of my article on the long term view still holds (thread here). And to add on, there has been discussion of a $3.5 trillion reconciliation bill on top of the infrastructure bill.

Rather than a hawkish Fed, we have a dovish one. And yet the yield curve flattened and the dollar up as expected. I see this similar to Q3 2020 where there were fears of the economy rolling over again from a second wave of Covid Lockdowns. This marked the bottom of commodities and commodity equites, the bottom of the 10 year yield, and in general the beginning of the reflation trade.

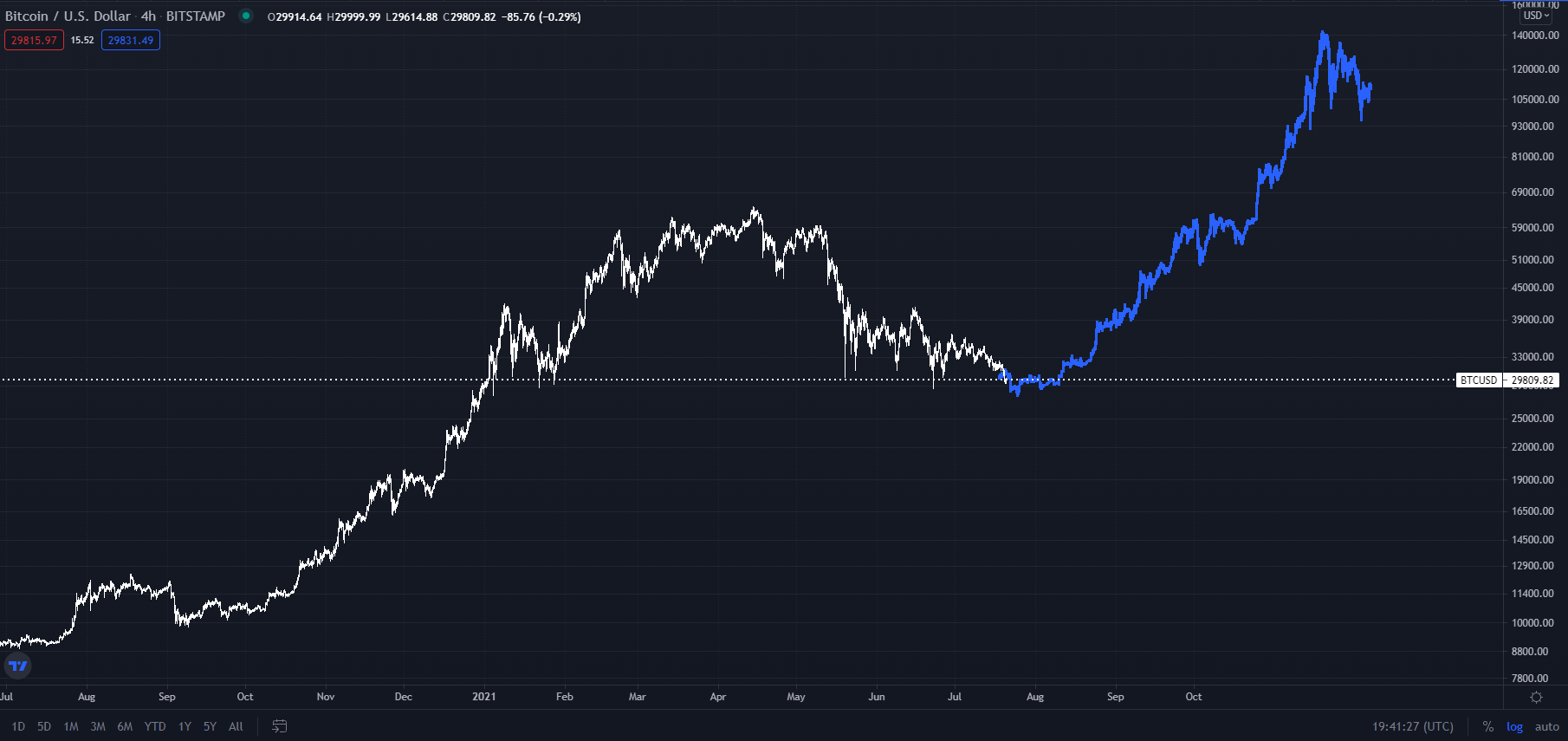

This is where I will looking for entries on long commodity equites, short dollar, and long cryptocurrencies (proxy being Bitcoin).

Below I take the fractals from the Q3 2020 timeframe to gauge market direction:

DXY

XLE

TLT

BTC

I am starting to develop a view that Bitcoin in the macro environment acts like the tail end of a whip. And the whip being risk-on in financial markets. However this view is not fully developed and I’ll share when complete.

Additionally on this view, it aligns well with tech performing well in deflationary environments and BTC in reflationary, high liquidity environments. Below is a thread that explains this well and it is aligning with the above view of reflation:

What to Watch

Yield Curve - do we see more flattening despite dovishness from the Fed

Federal Reserve narrative

Commodities and other Reflation stocks - back up?

Delta Variant - may be cause for concern. Yet when I go outside, I see NYC not slowing down so I am not worried about it. However it could develop negatively faster than expected. TBD on this.