Bitcoin & Risk On/Off Macro Dynamics

Bitcoin and the entire crypto market is a very speculative asset class. And under this feature, Bitcoin has shown to historically crash and top before other assets classes.

It is almost as if bitcoin is the last speculative frenzy and first to get washed out - as one would expect as you go down more speculative assets. As risk on develops in the market place, it first goes into least risky assets and to the most risky. A broad idea of this would be from treasuries to IG bonds to HY Bonds to Large-Cap Equities to Small-Cap Equities and finally to crypto.

Related Articles:

Seasonality

Here is the seasonality of the S&P 500 compared to bitcoin (excludes 2020):

My view of this seasonality has to do with the macro risk-on/off dynamics. The best way to view this is the analogy of a tide.

Water comes in (risk on) raising all asset prices. The riskiest assets are closest to shore. As the tide comes in, the less risky assets get wet and under water first and the riskiest last. As the tides comes in, more water (or market strength) is on top of less risk assets. Aka they are already wet and there fore the price is stronger but the risk on doesn’t impact the price as much. This is where the equity market decelerates and riskier assets including bitcoin start to outperform.

Similarly, water goes out (risk off) lowering all asset prices. Riskiest assets hit the hardest first. Just like with bitcoin finding a bottom before the equity market in almost all cases.

Lets look at several cases since 2016

Mid Summer 2017

Mid Cycle Bull Market

S&P stalled in late Q1/ early Q2 2017

Bitcoin started showing strength in Q2 2017

Reverse occurred over the summer

End of Year 2017

2017 Bitcoin Top and S&P topped a month later

Bitcoin topped prior to the S&P (Dec. 2017 and Jan. 2018) and had a cyclical bottom prior to S&P (Feb. 2018)

End of Year 2018

Bitcoin bottomed several weeks before S&P in Dec. 2018

Bitcoin crash occurred in Nov. 2018

Federal Reserve was in the middle of Quantitative Tightening and December 2018 was when the famous Powell Pivot occurred (here)

2019 BTC Cycle

Q2 2019, BTC rises as S&P wains

Beginning of July 2019, BTC tops while S&P marches up

The BTC top and crash occurs before the S&P bottoms in August 2019

S&P outperforms Bitcoin for the rest of year. At no point after the BTC top, did the S&P slow down

Q1 2020

S&P starts to decelerate and bitcoin heads up in a risk on environment

Bitcoin topped ~1 week before the S&P did

Covid crash occurs in March 2020. Bitcoin bottoms several days before S&P, even before the Fed came in with $3 trillion of QE

Reflation of Markets after Covid Crash

S&P gained traction prior to bitcoin in the summer

Once S&P started to accelerate up in Q3 2020, bitcoin started its climb

S&P started decelerating in Q1 2021 right as Bitcoin took off. Bitcoin doubled in Q1 2021

Current Backdrop

Bitcoin crashed in May 2021.

S&P didn’t have a drop like other cases (at least one worth noting)

The summer lull has been defined as usual. S&P reflating. Bitcoin flat and finding a bottom

As we are in Q3, we have the S&P decelerating and bitcoin accelerating back up, already 50% above the July 20th bottom

Macro Drivers

The seasonality research is all well and good, but its not bullet proof. Especially when we consider other macro dynamics at play.

30 Year Treasury Rates vs Bitcoin

30 year rates vs Bitcoin since Q2 2020 has shown a very high correlation. This is in line with the idea the rates up is risk on, and rates down is risk off

The correlation is also showing that bitcoin is coming a more mature macro asset classes. The rates correlation was not as strong in previous cycles.

Quantitative Tightening

But what is different from the 2017 is QE. In 2017, the Fed was keeping the balance sheet flat. Today, they are doing $120bn/month.

Stocks haven’t gone down with crypto yet but similar to Summer 2017 (drawdown?). And while the Federal Reserve is doing $120bn per month of QE. We did not have this in 2017. In fact the Fed was doing neither QE or QT and in process of beginning QT.

Below is the Federal Reserve Balance Sheet (blue) against bitcoin and the Bitwise fund Top 100 Crypto Fund.

In the 2013 and current cycles, QE was going on. Bitcoin topped right before QE ended.

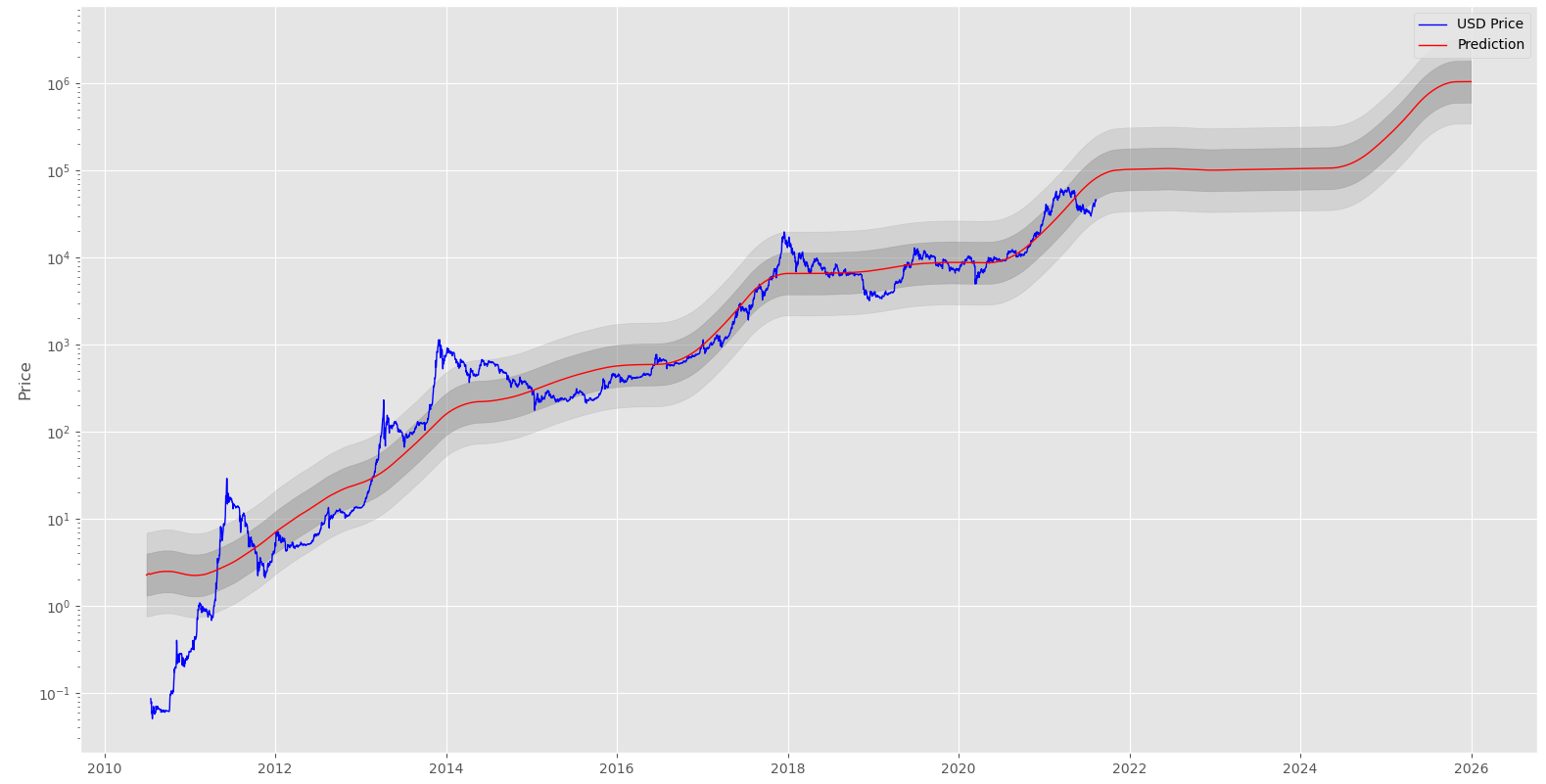

2017 did not have QE going on yet price ran up. This is most likely the cause of the bitcoin halving where the inflation rate of bitcoin is cut in half. For reference, here is my stock-to-flow model (based on PlanB model).

Current Model Estimates:

USD Price (Current / Model Price): $45,489 / $81,248

Market Capitalization: $854bn / $1,526bn

For reference, the 2013 and current bull cycles also had halvings. And 2013 outperformed the 2017 cycle. This potentially could have been because of the halving plus QE.

Conclusion

Effectively, Bitcoin is showing itself as a growing asset classes that is reaching the level of macro importance. Just look at the correlation with the 30 year. Late stages of risk-on are when to expect BTC and all other crypto assets to top. And they will be the first to bottom.

Given the seasonality, bull cycle similarities, and macro environment for bitcoin, I believe we will see a cycle similar to 2013 but longer than both the 2013 and 2017 cycles. Likely with a blow off top by year end at the earliest and Q1 2022 likeliest if the bitcoin cycle holds.

Here are some of my favorite bitcoin charts comparing today’s bull cycle to 2013’s.

This chart shows the cycles timing. Currently, we are set for a 75 week bull run starting at the bottom in late 2019 and ending late October. I don’t see how the cycle will hold like the previous too but it’ll probably be close.

Concerns

I’ll end with we should watch out for the Federal Reserve discussing tapering. It is unclear how tapering will impact asset prices including bitcoin.

The Fed has been saying employment data will be key for their decision on tapering. And the latest employment report beat expectations where (i) nonfarm payrolls rose by 943,000 in July, better than the 845,000 Dow Jones estimate and (ii) the unemployment rate slid to 5.4%, compared with the 5.7% expectation. There is a good chance the Fed will attempt, at minimum, mentioning plans to slowly taper.

Jobs Strength Leaves Fed and Powell With Nowhere to Hide - Bloomberg

And in a recent interview on Odd Lots, it seems there is strong debate on tapering.

“I would be supportive of adjusting these purchases soon, but once we start the adjustment process, I would probably prefer to have it be more gradual,” Kaplan said in an interview this week with Joe Weisenthal and Tracy Alloway on Bloomberg’s “Odd Lots” podcast.

Time will tell. Jackson Hole meeting anyone?

Authored by Derman Capital (Twitter)